This is a very short post that will be very useful to help you quickly set up your COVID-19 datasets. I’m sharing code at the end of this post that scrapes through all CSV datasets made available by COVID19-India API.

We have exposed all the crowdsourced patient details, travel history (published by authorities) and statewise trends in this live API : https://t.co/tNyhpPYTJD A shout-out to all Data Analysts, Planners and Enthusiasts to use this data for helping the containment efforts. @_mekin

Copy paste this standalone script into your R environment and get going!

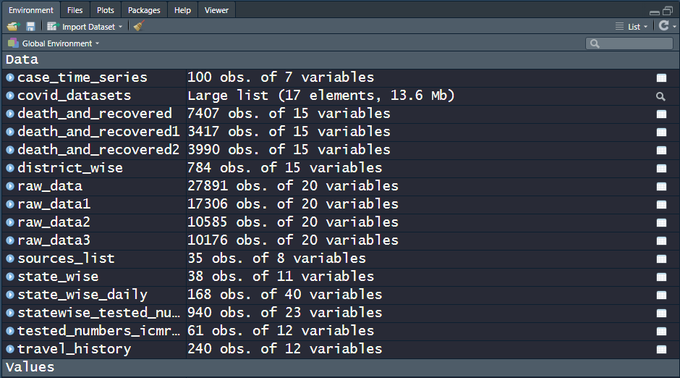

There are 15+ CSV files on the India COVID-19 API website. raw_data3 is actually a live dataset and more can be expected in the days to come, which is why a script that automates the data sourcing comes in handy. Snapshot of the file names and the data dimensions as of today, 100 days since the first case was recorded in the state of Kerala —

My own analysis of the data and predictions are work-in-progress, going into a Github repo. Execute the code below and get started analyzing the data and fighting COVID-19!

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

This post comes out of the blue, nearly 2 years since my last one. I realize I’ve been lazy, so here’s hoping I move from an inertia of rest to that of motion, implying, regular and (hopefully) relevant posts. I also chanced upon some wisdom while scrolling through my Twitter feed:

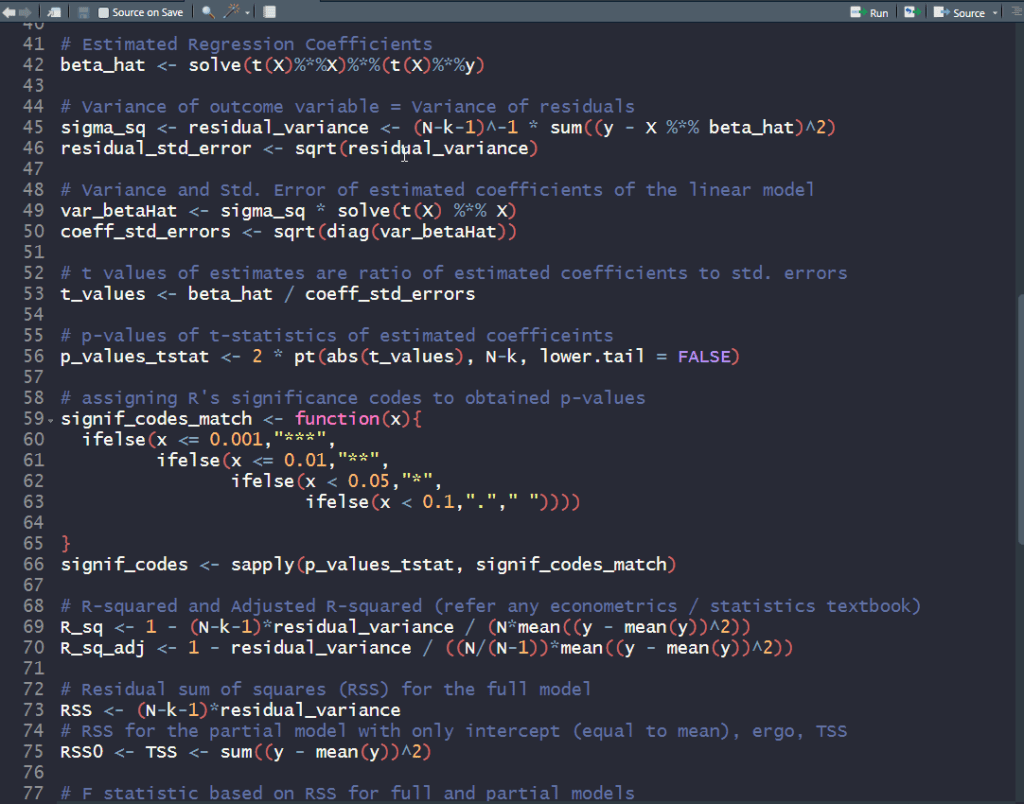

This blog post in particular was meant to be a reminder to myself and other R users that the much used lm() function in R (for fitting linear models) can be replaced with some handy matrix operations to obtain regression coefficients, their standard errors and other goodness-of-fit stats printed out when summary() is called on an lm object.

Linear regression can be formulated mathematically as follows: ,

is the outcome variable and is the data matrix of independent predictor variables (including a vector of ones corresponding to the intercept). The ordinary least squares (OLS) estimate for the vector of coefficients is:

The covariance matrix can be obtained with some handy matrix operations:

given that

The standard errors of the coefficients are basically and with these, one can compute the t-statistics and their corresponding p-values.

Lastly, the F-statistic and its corresponding p-value can be calculated after computing the two residual sum of squares (RSS) statistics:

– for the full model with all predictors

– for the partial model () with the outcome observed mean as estimated outcome

I wrote some R code to construct the output from summarizing lm objects, using all the math spewed thus far. The data used for this exercise is available in R, and comprises of standardized fertility measures and socio-economic indicators for each of 47 French-speaking provinces of Switzerland from 1888. Try it out and see for yourself the linear algebra behind linear regression.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

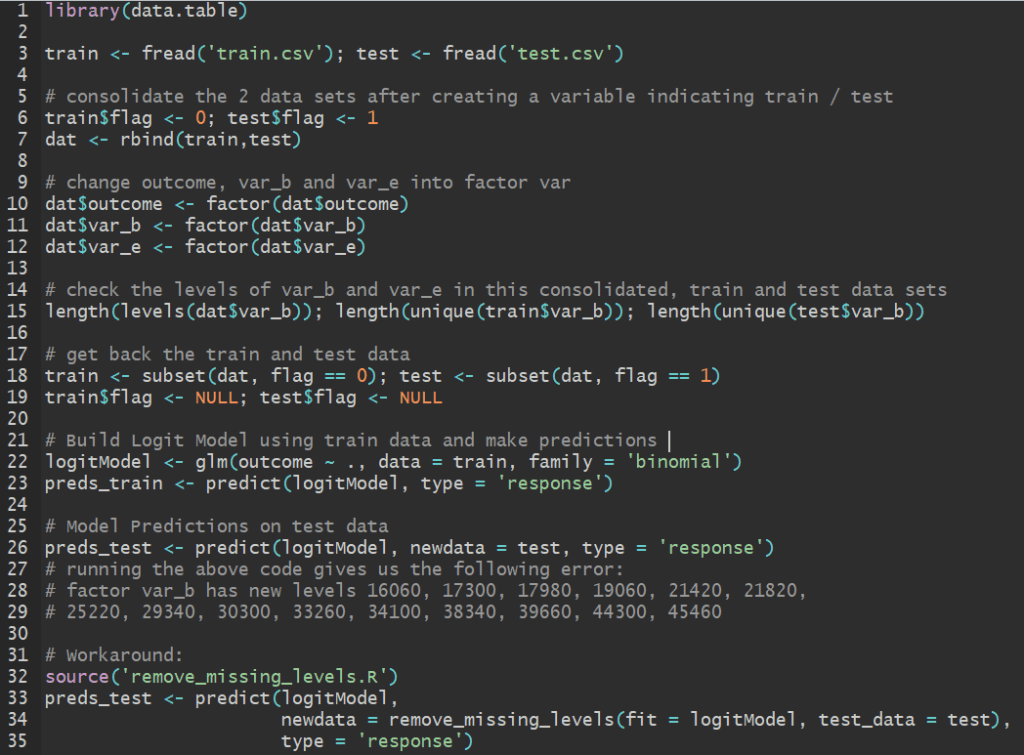

Let’s say you have data containing a categorical variable with 50 levels. When you divide the data into train and test sets, chances are you don’t have all 50 levels featuring in your training set.

This often happens when you divide the data set into train and test sets according to the distribution of the outcome variable. In doing so, chances are that our explanatory categorical variable might not be distributed exactly the same way in train and test sets – so much so that certain levels of this categorical variable are missing from the training set. The more levels there are to a categorical variable, it gets difficult for that variable to be similarly represented upon splitting the data.

Take for instance this example data set (train.csv + test.csv) which contains a categorical variable var_b that takes 349 unique levels. Our train data has 334 of these levels – on which the model is built – and hence 15 levels are excluded from our trained model. If you try making predictions on the test set with this model in R, it throws an error: factor var_b has new levels 16060, 17300, 17980, 19060, 21420, 21820,

25220, 29340, 30300, 33260, 34100, 38340, 39660, 44300, 45460

If you’ve used R to model generalized linear class of models such as linear, logit or probit models, then chances are you’ve come across this problem – especially when you’re validating your trained model on test data.

The workaround to this problem is in the form of a function, remove_missing_levels that I found here written by pat-s. You need magrittr library installed and it can only work on lm, glm and glmmPQL objects.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

Once you’ve sourced the above function in R, you can seamlessly proceed with using your trained model to make predictions on the test set. The code below demonstrates this for the data set shared above. You can find these codes in one of my github repos and try it out yourself.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

I recently bought a new laptop and began installing essential software all over again, including R of course! And I wanted all the libraries that I had installed in my previous laptop. Instead of installing libraries one by one all over again, I did the following:

Step 1: Save a list of packages installed in your old computing device (from your old device).

This saves information on installed packages in a csv file named installed_previously.csv. Now copy or e-mail this file to your new device and access it from your working directory in R.

Step 2: Create a list of libraries from your old list that were not already installed when you freshly download R (from your new device).

We now have a list of libraries that were installed in your previous computer in addition to the R packages already installed when you download R. So you now go ahead and install these libraries.

Step 3: Download this list of libraries.

install.packages(toInstall)

That’s it. Save yourself the trouble installing packages one-by-one all over again.

The most conventional approach to determine structural breaks in longitudinal data seems to be the Chow Test.

From Wikipedia,

The Chow test, proposed by econometrician Gregory Chow in 1960, is a test of whether the coefficients in two linear regressions on different data sets are equal. In econometrics, it is most commonly used in time series analysis to test for the presence of a structural break at a period which can be assumed to be known a priori (for instance, a major historical event such as a war). In program evaluation, the Chow test is often used to determine whether the independent variables have different impacts on different subgroups of the population.

As shown in the figure below, regressions on the 2 sub-intervals seem to have greater explanatory power than a single regression over the data.

For the data above, determining the sub-intervals is an easy task. However, things may not look that simple in reality. Conducting a Chow test for structural breaks leaves the data scientist at the mercy of his subjective gaze in choosing a null hypothesis for a break point in the data.

Instead of choosing the breakpoints in an exogenous manner, what if the data itself could learn where these breakpoints lie? Such an endogenous technique is what Bai and Perron came up with in a seminal paper published in 1998 that could detect multiple structural breaks in longitudinal data. A later paper in 2003 dealt with the testing for breaks empirically, using a dynamic programming algorithm based on the Bellmanprinciple.

I will discuss a quick implementation of this technique in R.

Brief Outline:

Assuming you have a ts object (I don’t know whether this works with zoo, but it should) in R, called ts. Then implement the following:

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

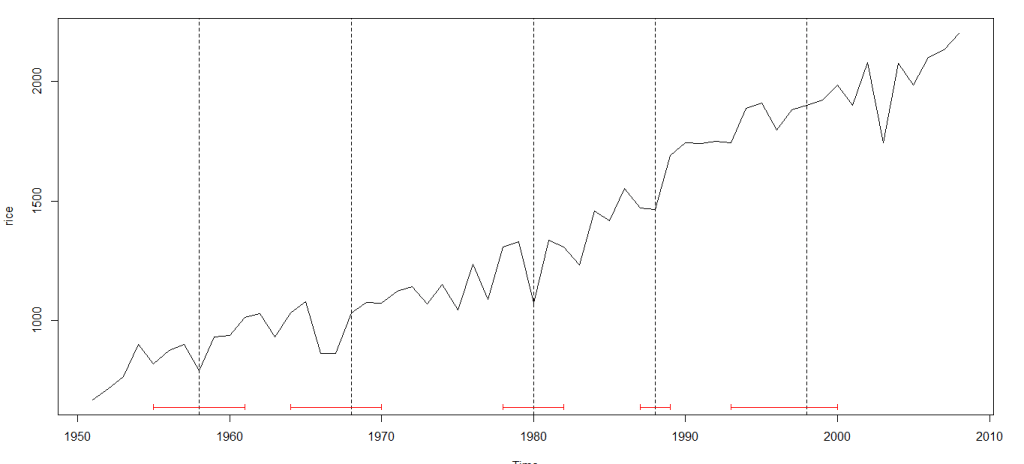

I started with data on India’s rice crop productivity between 1950 (around Independence from British Colonial rule) and 2008. Here’s how it looks:

You can download the excel and CSV files here and here respectively.

Here’s the way to go using R:

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

I am auditing this course currently and just completed its 2nd assignment. It’s probably one of the best courses out there to learn R in a way that you go beyond the syntax with an objective in mind – to do analytics and run machine learning algorithms to derive insight from data. This course is different from machine learning courses by say, Andrew Ng in that this course won’t focus on coding the algorithm and rather would emphasize on diving right into the implementation of those algorithms using libraries that the R programming language already equips us with.

Take a look at the course logistics. And hey, they’ve got a Kaggle competition!

There’s still time to enroll and grab a certificate (or simply audit). The course is offered once a year. I met a bunch of people who did well at a data hackathon I had gone to recently, who had learned the ropes in data science thanks to Analytics Edge.

Edit: This post is in its infancy. Work is still ongoing as far as deriving insight from the data is concerned. More content and economic insight is expected to be added to this post as and when progress is made in that direction.

This is an attempt to detect structural breaks in China’s FX regime using Frenkel Wei regression methodology (this was later improved by Perron and Bai). I came up with the motivation to check for these structural breaks while attending a guest lecture on FX regimes by Dr. Ajay Shah delivered at IGIDR. This is work that I and two other classmates are working on as a term paper project under the supervision of Dr. Rajeswari Sengupta.

The code below can be replicated and run as is, to get same results.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

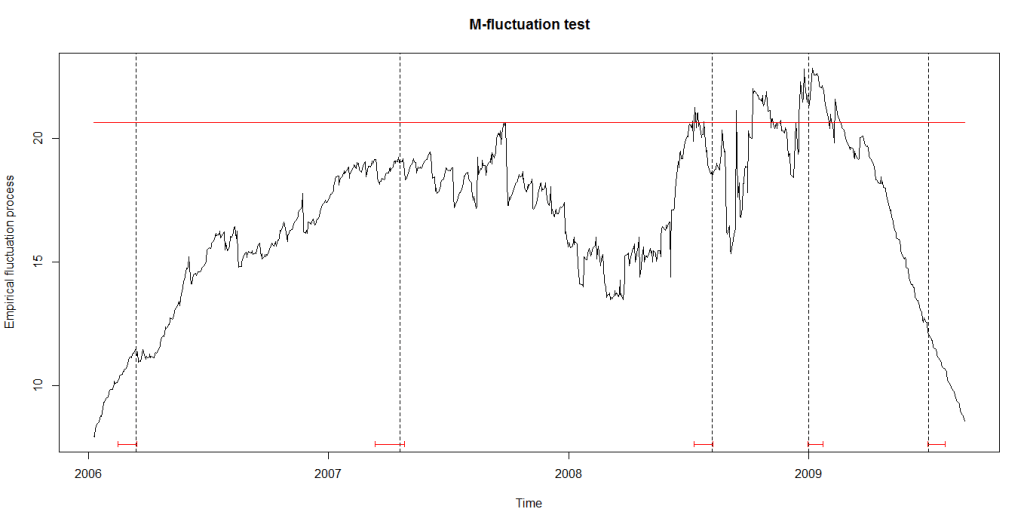

As can be seen in the figure below, the structural breaks correspond to the vertical bars. We are still working on understanding the motivations of China’s central bank in varying the degree of the managed float exchange rate.

EDIT (May 16, 2016):

The code above uses data provided by the package itself. If you wished to replicate this analysis on data after 2010, you will have to use your own data. We used Quandl, which lets you get 10 premium datasets for free. An API key (for only 10 calls on premium datasets) is provided if you register there. Foreign exchange rate data (2000 onward till date) apparently, is premium data. You can find these here.

Here are the (partial) results and code to work the same methodology on the data from 2010 to 2016:

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

We got breaks in 2010 and in 2015 (when China’s stock markets crashed). We would have hoped for more breaks (we can still get them), but that would depend on the parameters chosen for our regression.

This happens to be my 50th blog post – and my blog is 8 months old.

🙂

This post is the third and last post in in a series of posts (Part 1 – Part 2) on data manipulation with dlpyr. Note that the objects in the code may have been defined in earlier posts and the code in this post is in continuation with code from the earlier posts.

Although datasets can be manipulated in sophisticated ways by linking the 5 verbs of dplyr in conjunction, linking verbs together can be a bit verbose.

Creating multiple objects, especially when working on a large dataset can slow you down in your analysis. Chaining functions directly together into one line of code is difficult to read. This is sometimes called the Dagwood sandwich problem: you have too much filling (too many long arguments) between your slices of bread (parentheses). Functions and arguments get further and further apart.

The %>% operator allows you to extract the first argument of a function from the arguments list and put it in front of it, thus solving the Dagwood sandwich problem.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

group_by() defines groups within a data set. Its influence becomes clear when calling summarise() on a grouped dataset. Summarizing statistics are calculated for the different groups separately.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

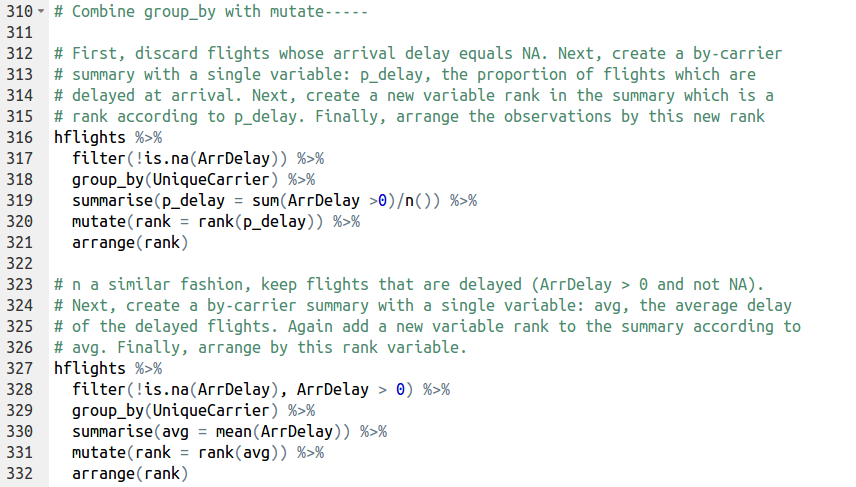

group_by() can also be combined with mutate(). When you mutate grouped data, mutate() will calculate the new variables independently for each group. This is particularly useful when mutate() uses the rank() function, that calculates within group rankings. rank() takes a group of values and calculates the rank of each value within the group, e.g.

rank(c(21, 22, 24, 23))

has output

[1] 1 2 4 3

As with arrange(), rank() ranks values from the largest to the smallest and this behaviour can be reversed with the desc() function.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

So after 8 months of playing around with R and Python and blog post after blog post, I found myself finally hacking away at a problem set from the 17th storey of the Hindustan Times building at Connaught Place. I had entered my first ever data science hackathon conducted by Analytics Vidhya, a pioneer in analytics learning in India. Pizzas and Pepsi were on the house. Like any predictive analysis hackathon, this one accepted unlimited entries till submission time. It was from 2pm to 4:30pm today – 2.5 hours, of which I ended up wasting 1.5 hours trying to make my first submission which encountered submission error after submission error until the problem was fixed finally post lunch. I had 1 hour to try my best. It wasn’t the best performance, but I thought of blogging this experience anyway, as a reminder of the work that awaits me. I want to be the one winning prize money at the end of the day.

Note that this post is in continuation with Part 1 of this series of posts on data manipulation with dplyr in R. The code in this post carries forward from the variables / objects defined in Part 1.

In the previous post, I talked about how dplyr provides a grammar of sorts to manipulate data, and consists of 5 verbs to do so:

The 5 verbs of dplyr select – removes columns from a dataset filter – removes rows from a dataset arrange – reorders rows in a dataset mutate – uses the data to build new columns and values summarize – calculates summary statistics

I went on to discuss examples using select() and mutate(). Let’s now talk about filter(). R comes with a set of logical operators that you can use inside filter(). These operators are: x < y,TRUE if x is less than y x <= y, TRUE if x is less than or equal to y x == y, TRUE if x equals y x != y, TRUE if x does not equal y x >= y, TRUE if x is greater than or equal to y x > y, TRUE if x is greater than y x %in% c(a, b, c), TRUE if x is in the vector c(a, b, c)

The following call, for example, filters df such that only the observations where the variable a is greater than the variable b: filter(df, a > b)

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

Combining tests using boolean operators

R also comes with a set of boolean operators that you can use to combine multiple logical tests into a single test. These include & (and), | (or), and ! (not). Instead of using the & operator, you can also pass several logical tests to filter(), separated by commas. The following calls equivalent:

filter(df, a > b & c > d) filter(df, a > b, c > d)

The is.na() will also come in handy very often. This expression, for example, keeps the observations in df for which the variable x is not NA:

filter(df, !is.na(x))

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

Arranging Data arrange() can be used to rearrange rows according to any type of data. If you pass arrange() a character variable, R will rearrange the rows in alphabetical order according to values of the variable. If you pass a factor variable, R will rearrange the rows according to the order of the levels in your factor (running levels() on the variable reveals this order).

By default, arrange() arranges the rows from smallest to largest. Rows with the smallest value of the variable will appear at the top of the data set. You can reverse this behaviour with the desc() function. arrange() will reorder the rows from largest to smallest values of a variable if you wrap the variable name in desc() before passing it to arrange()

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

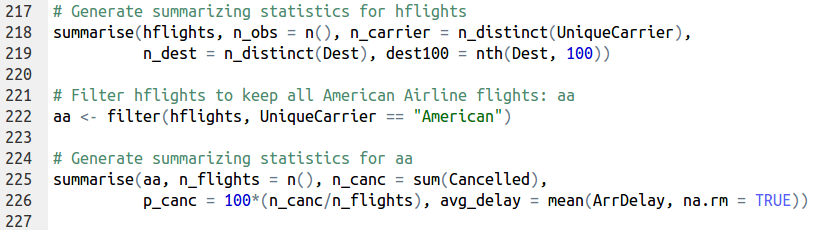

summarise(), the last of the 5 verbs, follows the same syntax as mutate(), but the resulting dataset consists of a single row instead of an entire new column in the case of mutate().

In contrast to the four other data manipulation functions, summarise() does not return an altered copy of the dataset it is summarizing; instead, it builds a new dataset that contains only the summarizing statistics.

Note:summarise() and summarize() both work the same!

You can use any function you like in summarise(), so long as the function can take a vector of data and return a single number. R contains many aggregating functions. Here are some of the most useful:

min(x) – minimum value of vector x. max(x) – maximum value of vector x. mean(x) – mean value of vector x. median(x) – median value of vector x. quantile(x, p) – pth quantile of vector x. sd(x) – standard deviation of vector x. var(x) – variance of vector x. IQR(x) – Inter Quartile Range (IQR) of vector x. diff(range(x)) – total range of vector x.

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

dplyr provides several helpful aggregate functions of its own, in addition to the ones that are already defined in R. These include:

first(x) – The first element of vector x. last(x) – The last element of vector x. nth(x, n) – The nth element of vector x. n() – The number of rows in the data.frame or group of observations that summarise() describes. n_distinct(x) – The number of unique values in vector x

This file contains hidden or bidirectional Unicode text that may be interpreted or compiled differently than what appears below. To review, open the file in an editor that reveals hidden Unicode characters.

Learn more about bidirectional Unicode characters

This would be it for Part-2 of this series of posts on data manipulation with dplyr. Part 3 would focus on the pipe operator, Group_by and working with databases.

,

,

is the

is the  outcome variable and

outcome variable and  is the

is the  data matrix of independent predictor variables (including a vector of ones corresponding to the intercept). The ordinary least squares (OLS) estimate for the vector of coefficients

data matrix of independent predictor variables (including a vector of ones corresponding to the intercept). The ordinary least squares (OLS) estimate for the vector of coefficients  is:

is:

and with these, one can compute the t-statistics and their corresponding p-values.

and with these, one can compute the t-statistics and their corresponding p-values. – for the full model with all predictors

– for the full model with all predictors – for the partial model (

– for the partial model (![\mathbf{y} = \mathbf{\mu} + \mathbf{\nu}; \mathbf{\mu} = \mathop{\mathbb{E}}[\mathbf{y}]; \mathbf{\nu} \sim N(0, \sigma_0^2 \mathbf{I})](https://s0.wp.com/latex.php?latex=%5Cmathbf%7By%7D+%3D+%5Cmathbf%7B%5Cmu%7D+%2B+%5Cmathbf%7B%5Cnu%7D%3B+%5Cmathbf%7B%5Cmu%7D+%3D+%5Cmathop%7B%5Cmathbb%7BE%7D%7D%5B%5Cmathbf%7By%7D%5D%3B+%5Cmathbf%7B%5Cnu%7D+%5Csim+N%280%2C+%5Csigma_0%5E2+%5Cmathbf%7BI%7D%29+&bg=ffffff&fg=000&s=1&c=20201002) ) with the outcome observed mean as estimated outcome

) with the outcome observed mean as estimated outcome